Money is one of the few things that touches every aspect of family life—security, dreams, even relationships. Yet, it’s rarely talked about openly. Many families avoid discussing finances out of discomfort or fear of conflict, missing out on valuable opportunities to build understanding and stability together. When parents and children approach money as a shared responsibility, they don’t just improve their current situation—they rebuild your financial future as a family. The lessons learned and the habits formed can shape not just your household, but the next generation’s relationship with money.

The Family as a Financial Team

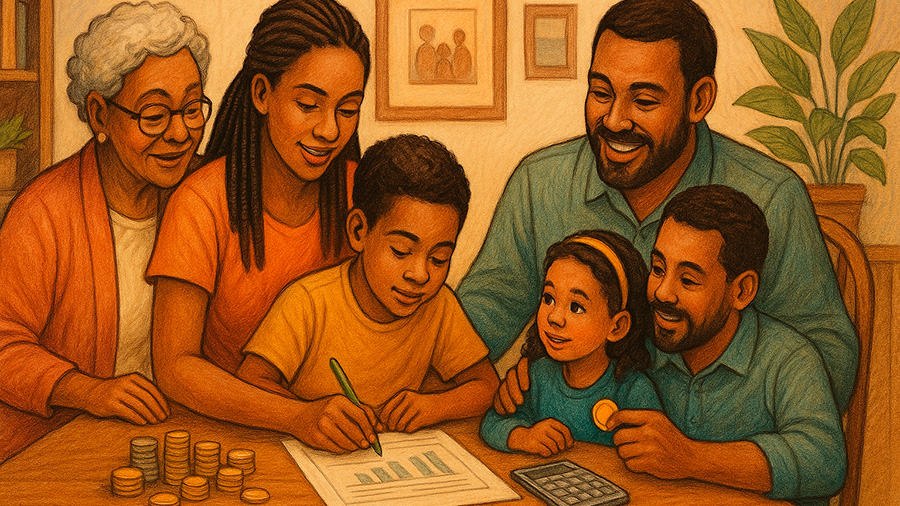

Families often view money management as an individual responsibility: parents earn, pay bills, and save, while kids remain unaware of what financial stability really requires. But when financial decisions are made collaboratively, a sense of unity and purpose emerges. Discussing budgets, debts, and goals helps transform money from a source of stress into a tool for growth. This teamwork approach allows you to rebuild your financial future with everyone invested in the outcome.

According to research from the American Psychological Association, financial stress is one of the top causes of tension within families. The irony is that the stress usually lessens once people begin communicating. Involving children in simple financial conversations—like planning vacations or comparing grocery prices—teaches transparency, accountability, and long-term thinking.

Teaching the Next Generation About Stability

Financial education starts at home. Schools rarely provide the depth of real-world money lessons children need. Parents who take the initiative give their kids a head start not just in earning, but in managing wealth responsibly. Understanding how to rebuild your financial future means passing down habits like saving early, using credit wisely, and balancing needs versus wants.

Practical Lessons for Kids and Teens

- Budgeting with purpose: Let kids manage a small allowance with clear goals, like saving for a toy or donating to charity.

- Explaining credit and debt: Show how borrowing can be useful—but only when done with a plan for repayment.

- Modeling savings habits: Set up a family savings jar for shared goals, such as a trip or a new piece of furniture.

- Discussing emergencies: Teach that saving for unexpected expenses prevents stress and debt later.

These habits might seem small, but they create a foundation of trust and competence. When children grow up seeing responsible money management in action, they learn that stability isn’t luck—it’s discipline.

Building a Shared Financial Vision

For adults, rebuilding financial stability often starts after a disruption—job loss, illness, debt, or poor investments. But a setback can also be the perfect opportunity for a reset. Bringing the family together to re-evaluate priorities creates unity and accountability. Everyone knows where the family stands, and what must be done to move forward.

How to Create a Family Financial Plan

- Set collective goals: Identify short-term and long-term aims—paying off a credit card, building an emergency fund, buying a home, or saving for college.

- Assign roles: Divide responsibilities. One person tracks spending, another compares insurance rates, another focuses on income growth.

- Establish a review routine: Hold monthly “money meetings” where progress is reviewed and adjustments are made.

- Celebrate milestones: Recognizing progress—no matter how small—reinforces positive behavior.

Financial planning isn’t about spreadsheets—it’s about creating a shared vision of what a good life looks like. That vision keeps families motivated even when sacrifices are required. The process of aligning on goals is itself an act of rebuilding trust and direction—a powerful way to truly rebuild your financial future.

Example of a Family Financial Goal Plan

| Goal | Timeline | Responsible Person(s) | Strategy |

|---|---|---|---|

| Pay off credit card debt | 12 months | Parents | Redirect 10% of monthly income toward principal payments |

| Emergency fund | 6 months | Entire family | Save $100 per month; sell unused items online |

| College savings | Ongoing | Parents | Open 529 plan; contribute tax refunds |

| Family vacation fund | 9 months | All members | Save spare change and small bonuses |

Creating structure around financial goals ensures clarity and accountability. Everyone knows their role, and progress feels tangible. It’s one of the simplest, most effective ways to rebuild momentum after financial hardship.

Communication: The Secret to Long-Term Success

Honest communication transforms financial chaos into progress. Many families avoid discussing money until there’s a crisis—missed bills, credit issues, or a loss of income. Yet regular check-ins can prevent those crises entirely. Talking about money shouldn’t feel like a punishment; it should feel like teamwork.

Tips for Healthy Money Conversations

- Stay judgment-free: Focus on facts, not blame. Everyone makes mistakes; the key is to learn from them.

- Use “we” language: Phrases like “We need to cut back” create unity instead of conflict.

- Share progress, not just problems: Celebrate savings milestones and small wins to build motivation.

- Involve kids in age-appropriate ways: Even young children can learn the basics of saving and giving.

Open communication builds emotional stability, which in turn supports financial stability. When family members feel heard and respected, cooperation becomes natural—and that cooperation is what helps you rebuild your financial future more effectively than any financial product ever could.

Generational Wealth: Thinking Beyond Today

Building wealth isn’t just about making more money—it’s about preserving and multiplying what you already have. Families that communicate about money are better positioned to pass on financial literacy, assets, and opportunities. That’s how generational wealth starts—not just with inheritances, but with knowledge and habits that compound over time.

| Generation | Focus | Financial Goal | Key Habit |

|---|---|---|---|

| Parents | Stability | Pay down debt and build savings | Consistent budgeting and expense tracking |

| Teens | Education | Build credit safely, avoid unnecessary debt | Using secured cards or co-signed accounts responsibly |

| Children | Awareness | Understand value, giving, and delayed gratification | Saving and discussing money openly |

Each generation has a role to play. The habits parents model become the foundation their children build upon. Over time, this creates not just financial security, but emotional resilience and mutual respect—a true legacy.

When Financial Setbacks Happen

No family’s financial journey is smooth. There will be setbacks—unexpected expenses, job losses, or market downturns. The key is response, not perfection. Families that prepare mentally and financially bounce back faster. Setting up emergency savings, diversifying income sources, and staying debt-aware create the cushion needed to weather storms.

Remember, rebuilding isn’t about perfection—it’s about progress. Even if you make one positive financial decision a month, you’re already on the right track. Each choice compounds, each step matters. The momentum itself becomes a form of motivation.

Rebuilding Together Is the Real Wealth

When a family learns to manage money collectively, something powerful happens. The process strengthens relationships, fosters mutual respect, and plants seeds for future generations. True wealth isn’t just measured in dollars—it’s measured in shared goals, communication, and stability. Every honest conversation, every small victory, every decision made together helps you rebuild your financial future not as individuals, but as a united team. And that unity, more than any investment or income, is what creates lasting financial peace.